You've come to the right place if you've been looking for a Yotta app review to see if this savings platform is safe. This isn't a normal review of an app—it's a full account of one of the biggest fintech disasters of the decade, told through court documents, federal filings, and the real-life experiences of users who are still waiting for answers almost two years later.

What does the Yotta app do? It's a prize-linked savings platform that made saving money fun, and for a long time, people really liked using it. The short answer to the question "Is the Yotta app real?" is not easy. The platform was real. The problems that came after were also very real. This is all the information you need.

What Is the Yotta App?

Yotta started out as a new kind of savings account that was different from the usual ones. The idea was simple: put your money in, earn interest, and get lottery-style prize entries based on how much money you had. You got more prize tickets the more you saved. It was like a savings account that made saving for an emergency feel like a game.

Yotta marketed itself as a fun way to save money with lottery-style prizes.

Yotta marketed itself as a fun way to save money with lottery-style prizes.

At its peak, the Yotta savings app had about 85,000 users who had put in more than $112 million in total. Users thought the app was a real financial product that was insured by the FDIC.

Yotta was a fintech company, which means it wasn't a bank. Instead, it used Synapse Financial Technologies, a third-party middleware company, to connect user accounts to its banking partner, Evolve Bank & Trust. Fintech often uses this structure, which is known as Banking-as-a-Service (BaaS). This story shows that it's also very bad when something goes wrong.

The Timeline: How the Crisis Happened

April 22, 2024: The First Domino Falls

The middleware company that connects Yotta to its banking partners, Synapse Financial Technologies, filed for Chapter 11 bankruptcy. For most Yotta users, this was the first time they had ever heard of Synapse, a company that had been in the way of their money the whole time.

May 11, 2024: Lockout of All Accounts

Evolve Bank & Trust stopped processing payments for Yotta users just a few weeks after the Synapse bankruptcy. No more ACH transfers. There were no more wire transfers. Debit cards stopped working. Users woke up to find that all of their cashout methods were completely frozen.

Adam Moelis, the CEO of Yotta, said in public that 85,000 customers with $112 million in savings had been locked out of their accounts.

June 2024: The Money Goes Missing

At this point, things got very scary. In the Synapse bankruptcy case, court documents showed that eight banks held a total of $109 million in Yotta user funds as of April 2024. After the freeze, only $1.4 million was found about a month later.

Almost $96 million had gone missing from the books, and there was no clear record of where it went. The bankruptcy trustee later said that a full reconciliation might not be possible.

August 2024: Federal Regulators Step In

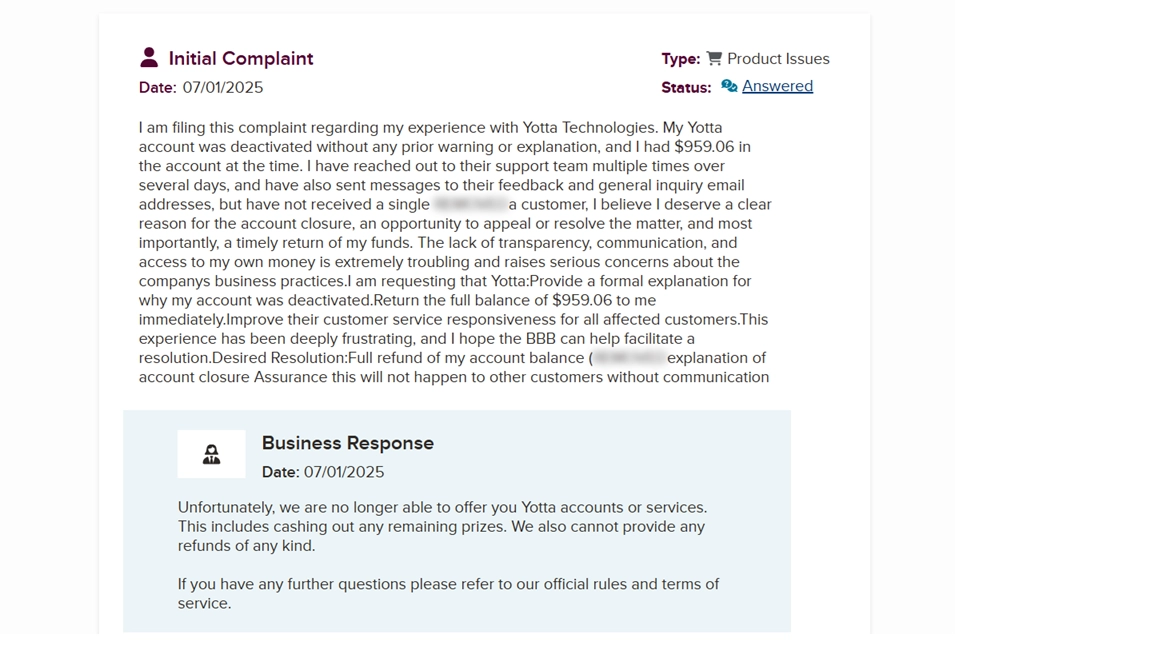

The Consumer Financial Protection Bureau (CFPB) sued Synapse and later agreed to a $46.2 million settlement from its Civil Penalty Fund to pay back the victims. Even though the settlement was approved, most Yotta users had not yet received their distributions by early 2026.

November 2024: Small, Unexplained Payments

Evolve Bank started sending small payments to some users, but the amounts were inconsistent and shockingly low compared to the balances in their accounts. Forbes reported that one author who put in $400 got nothing, while users who put in $30,000 or more got amounts in the single digits.

An Evolve witness said in a deposition that the bank "does not know how Ankura calculated the amount that each user was entitled to." This means that even Evolve couldn't explain how the payouts were figured out.

January 2026: Still Noticed Differences

Evolve said on January 8, 2026—607 days after freezing user funds—that it had found more money owed to users. This happened even though the bank said it had "completed" reconciliation in October 2024. Finding more differences made people even more suspicious of the accuracy of previous reconciliation reports.

February 2026: Users Not Allowed to Get Distributions

Evolve planned a distribution for February 2026, but Yotta users were not allowed to get any of the money. Users on Reddit in the r/yotta thread are trying to figure out why they are still locked out while Evolve says it has their money.

What the Court Papers Showed

Several things that came up in depositions and court filings give us important background information for understanding the whole situation:

Hank Word, the former president of Evolve, invoked his Fifth Amendment right against self-incrimination when he was asked during a deposition whether Yotta user funds were FDIC insured and whether certain actions had put that insurance coverage at risk. People in the U.S. can use the Fifth Amendment if they think that answering could make them liable for a crime.

Sealed Depositions: Evolve asked to seal some deposition transcripts because they contained "commercially sensitive" information. The motions are still part of the public court record.

These are not claims; they are facts that have been recorded in court. Anyone looking into this case can read the original filings to get the full picture.

Is the Yotta App Safe to Use Today?

If you're wondering if it's safe to put new money into the Yotta banking app right now, that's something you should really think about.

As of March 2026, this is what the public record says:

- 85,000 users still can't get to their money that they put in good faith.

- The app is still available on iOS and Android, but it has changed to focus on games and sweepstakes.

- The BBB gave Yotta a F rating, which is the worst grade they can give, and the company is not BBB accredited.

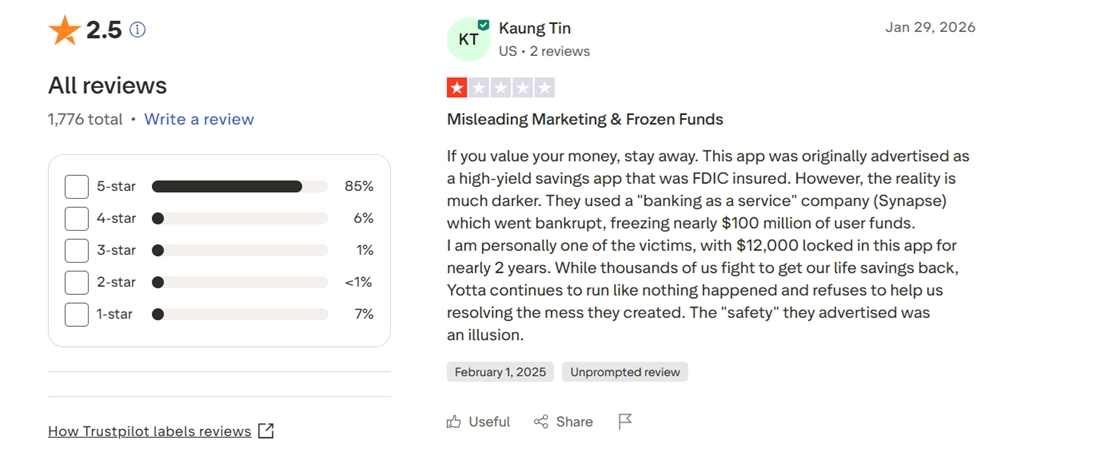

- Based on more than 3,270 reviews, Trustpilot gives it a 1.8 out of 5 star rating. Recent reviews mostly talk about the account freeze experience.

- It is expected that CFPB distributions will reach users between November 2026 and November 2027. This means that some users may have to wait three or more years from the original freeze date.

Yotta currently holds an F rating from the Better Business Bureau.

Yotta currently holds an F rating from the Better Business Bureau.

Trustpilot shows a 1.8/5 star rating based on over 3,270 reviews, with most recent reviews discussing the account freeze.

Trustpilot shows a 1.8/5 star rating based on over 3,270 reviews, with most recent reviews discussing the account freeze.

What This Means for People Who Use Fintech

It's not just one company's story about the Yotta situation. It's a case study in the structural risks that come with the Banking-as-a-Service model that powers many well-known fintech apps.

When you put money into a fintech app, you're not always putting it directly into a bank. You're putting money into a system with layers that includes:

- The fintech app (Yotta)

- A middleware business called Synapse

- A bank that works with Evolve

Every layer makes things more complicated. Every layer makes you wonder who is really in charge of your money when something goes wrong. The Yotta crisis showed what happens when that chain breaks: no one knows where the money went.

Apps Like Yotta: Safer Options to Think About

If you came here looking for apps like Yotta or apps that are similar to Yotta, the good news is that there are prize-linked savings options with clearer structures:

- Prizii lets you save money by linking it to prizes through federally insured credit unions.

- WinIt is a savings app with lottery-style drawings.

- Traditional high-yield savings accounts at banks that are members of the FDIC (no middleware layer)

If you're really interested in the prize part, you should look into credit union-based prize savings programs. They work directly through federally regulated institutions without any third-party middleware.

The Bottom Line: Is the Yotta App Real?

Yotta was a real product, but it was built on a shaky base. There were real deposits, real users, and a real prize-linked savings idea. The Synapse bankruptcy showed that the fintech infrastructure that Yotta and many other similar apps depended on had a structural weakness.

As of March 2026, tens of thousands of users are still waiting for a solution. The court case is still going on. Federal agencies are still involved. The legal process has not yet revealed the whole story of what happened to the missing money.

Key Lessons for Fintech Users

- Understand the structure. Before depositing money into any fintech app, research who the actual banking partner is and verify your FDIC insurance directly with that bank.

- Don't use fintech for emergency funds. Never rely on fintech apps for your emergency fund or long-term savings. Use established, directly-insured banks for these critical funds.

- Keep documentation. Screenshot your balances, save your statements, and maintain records of all deposits and withdrawals.

- Consider credit unions. For prize-linked savings, look for programs offered directly through federally insured credit unions rather than third-party fintech apps.

If you have money in a fintech savings app right now, this situation teaches you one clear and useful lesson: before you put a lot of money into any financial product, make sure you understand how it works. Find out who your real bank partner is, check with that bank directly to make sure your FDIC insurance is valid, and never use a fintech app instead of a real bank for your emergency fund or long-term savings.

The legal proceedings that will happen in the next few months should make the Yotta situation clearer. The facts that have been written down speak for themselves until then.

Frequently Asked Questions

Related Resources

Stay Informed About Your Money

Explore our comprehensive reviews of financial platforms and find safe, legitimate opportunities for your savings.

Compare Top Financial Platforms Now